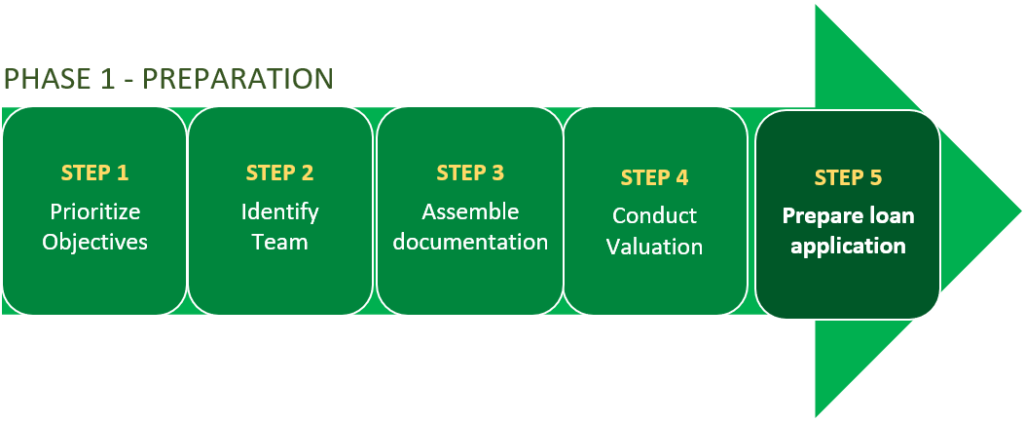

Prepare Loan Application

BorrowPQ helps you prepare a comprehensive loan application that can result in your application getting fast tracked with the lender. BorrowPQ includes sample and template documents that will accelerate the creation of the loan application.

The following documents are described with the critical aspects of what the lender is expecting from each.

Confidential Information Memo (CIM) / or “Teaser”

The teaser should impart a core summary of your business, your assets, and your borrowing requirements, including the planned use of funds. Keep it brief, preferably 1 page, or less!

BPQ Prequalified Asset Inventory & Valuation Report

The report includes the inventory and borrowing base valuation calculations, notes and assumptions that you have compiled for your Accounts Receivable, Inventory, Machinery and Equipment, and Commercial Real Estate. The report also includes the financial profile you compiled for Income & Expense, Assets & Liabilities, and Debt Schedule.

This provides an estimate of your borrowing base, which you can use to submit borrowing applications to BorrowPQ participating lenders. Your actual borrowing capacity will be subject to the review and underwriting criteria of the lender.

The CIM and BPQ Asset Inventory report are intended to be used for initial communications and determination of interest for a full application submission. See the Phase 2 activities outlined below and consider including these documents with your initial outreach.

BPQ Universal ABL Application

BorrowPQ provides participating borrowers a “universal” template for an ABL financing application. It is expected that this template will be completed in collaboration with prospective lenders.

BorrowPQ lenders will accept this document as part of your submission for screening and eligibility consideration. BorrowPQ lenders also often have their own format for application, and this template is intended to streamline the effort needed to copy/paste information into such formats.

The following elements are included in the template:

PRELIMINARY REVIEW SCREENING MEMORANDUM

NAME OF BORROWER:

OWNERSHIP STRUCTURE

- Proposed Borrower(s)

- Legal structure

- Company business activity description

- Current ownership details

- Personal guarantee availability

- Owners’ roles in business operations

- Plans, if any, to sell or pass down to next generation

PROPOSED LOAN STRUCTURE (included any special recommendations)

- Facility (Loan Amount being requested)

- Collateral being leveraged

- Proposed Advance Rates (by collateral type)

- Proposed Interest Rates (by collateral type)

- Proposed Fees

- Collateral Monitoring

- Closing

- Annual

- Early Termination

- Other

- Expected Return (ROA)

- Conditions of close

BUSINESS OVERVIEW

- Date founded/acquired; timeline, if necessary

- Description of business including industry, product lines, divisions, seasonality, special contractual arrangements, etc.

- Description of affiliated businesses

- Location of offices; manufacturing facilities;

distribution warehouses; other (e.g., processors)

- Full address of all locations and descriptions of facilities

MANAGEMENT TEAM

- Key members of management

- Years at company

- Industry and other relevant experience

- Education

- Board members

REASONS FOR REFINANCE/REQUEST

- Exiting a regulated bank

- Performance issues- covenant violations, other

- Forbearance agreement including maturity or special terms

- Lack of performance to qualify for bank financing

- First-time leverage/capital raise

CURRENT DEBT STRUCTURE

- Senior debt- balance outstanding, maturity, interest rate, collateral

- Current revolver tied to BBC [What is BBC?]

- Equipment or real estate loans -balance outstanding, maturity, interest rate

- Subordinated debt holders- Balance outstanding, maturity, interest rate

AVAILABLE COLLATERAL

- Accounts Receivable

- Revenue recognition

- Does the billing include any of the following?

- Billing in arrears

- Prebill (monthly, quarterly, annually, etc.)

- Other (guaranteed sales, consignment, subscription, etc.)

- Warranties

- Concentrations (>15%)

- Federal government (Assignment of Claims)

- Foreign (credit insured?)

- Inventory

- Description (breakdown of RM, WIP, FG, In-transit) [Do you need to define these terms? e.g. RM, FG, etc.?]

- Locations

- Leased or owned

- Currently under a landlord lien waiver

- 3rd party processor or warehouse

- Limitations on access to the inventory

- Tracking

- Perpetual system- how often updated?

- Physical counts – monthly, quarterly, annual, cycle counting

- Valuation

- Method (FIFO, LIFO, avg cost)

- Appraised value (if available)

- Turnover

- Slow moving/obsolete

- Exam Test TBD

- Exam Test TBD

- Exam Test TBD

- Machinery and Equipment

- Brief description (including age, concentration)

- Appraised value (if available)

- Request for future Capital Expenditures (CapEx)

- Commercial Real Estate (Copy for multiple

buildings)

- Owned by business or separate entity (LP, LLC)

- Description of Property

- Appraised value, if any

- Mortgages, if any

- Any known environmental issues

BORROWING BASE

- Proforma Borrowing Base Certficate structure needed to refinance existing lenders including advances against M&E and/or real estate; estimate ineligibles;

- Include an estimated proforma sources and uses at closing

- Clean-up of past due payables closing

- Closing costs

- Initial working capital requirement

- Other (e.g. past due taxes, etc.)

FINANCIAL PERFORMANCE AND HISTORY

- Income Statement- historical; preferably audit

or review

- Brief description of prior two years performance (i.e. trends, etc.)

- Sales, gross profit, net income/loss, EBITDA

- Fixed charge coverage

- Current year-to-date performance including projected performance for the year

- Current plans to improve performance (e.g.

discontinue product line, cut costs (fixed or variable), sales initiatives,

margin enhancements, etc.)

- Projections- brief summary

- Balance Sheet

- Accounts Payable

- AP Turnover

- Identify any key vendors and alternative sources

- Terms (e.g. COD)

- Total and amount >90 days

- Held checks

- Accrued expenses (e.g. past due payroll, p/r taxes, other taxes, rent)

CASH

- Current Accounts used/where

- Reconciliation of accounts

TAXES

- Payroll

- Property

- Sales

INSURANCE

- List of coverage and amounts

CREDIT RISKS AND PROPOSED MITIGANTS (examples)

- Financial reporting limitations, if any

- Over advance- Seasonality need or other

- Commodity pricing, impact of tariffs, etc.

- Significant affiliate and/or related party transactions

- Stretched payables

- Past due payroll or other taxes

OTHER

- Recommend additional reporting items (e.g. 13-week cash flow)

- Payment plans (e.g. IRS)

- Outstanding litigation

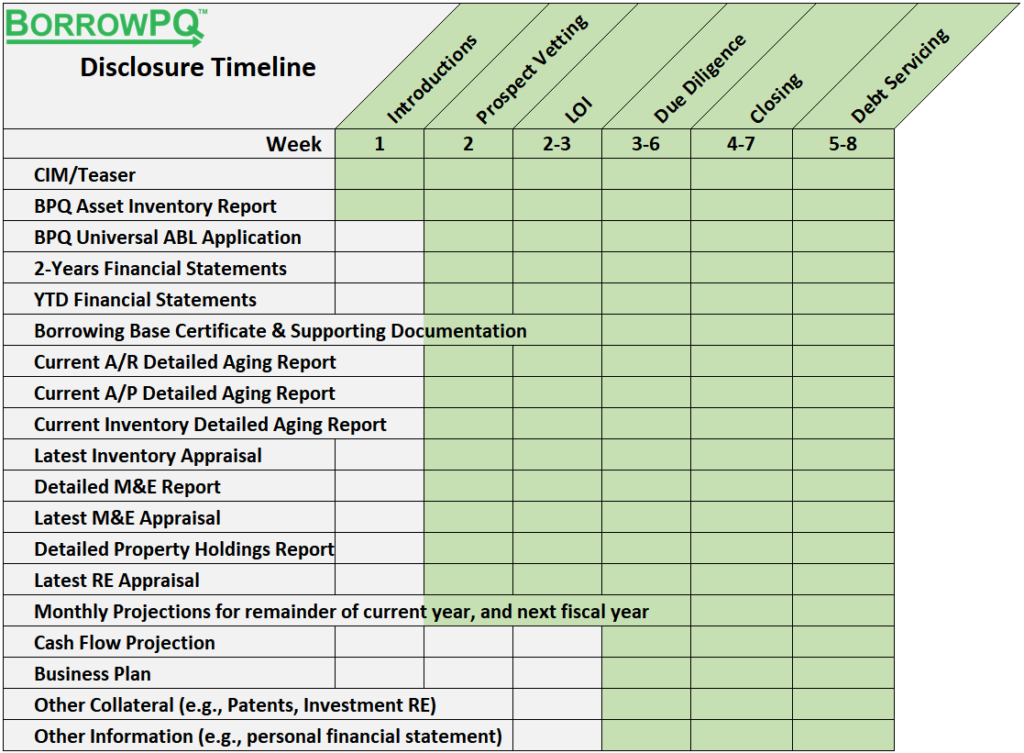

BPQ Documentation and High-Level Disclosure Timeline

The following graphic summarizes typical original documentation requirements for ABL lenders, as well as the expected timing of them in the loan application process:

PQ can refer you to third-party advisors for Step 5 including Management Consultants, Tax Consultants, Lawyers, Accountants and more.

Contact Us at any time for help or to provide feedback